Please note, all references to “CBD” or “CBD products” within this post refers to hemp-derived CBD, not marijuana-derived CBD.

Hemp-derived CBD products: you can’t avoid them anymore. From the CBD edibles at your local pharmacy to the hemp moisturizing skin cream in your mother’s bathroom, CBD products are on their way to attaining an almost ubiquitous role in contemporary life.

Thanks in part to the 2018 Farm Bill, which federally legalized industrial hemp plants from which CBD can be extracted, the floodgates have been opened for the entire CBD and hemp industry.

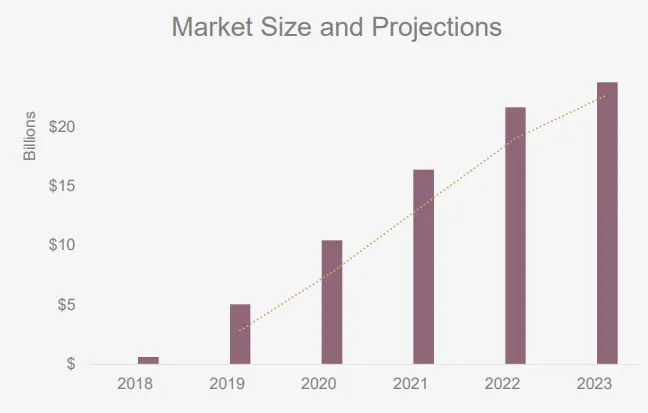

In fact, analysts predict consumer sales of U.S. CBD products to rise from $620 million in 2018 to $23.7 billion by 2023.

The potential revenue of CBD sales could experience a vast increase thanks to the legalization of industrial hemp in the 2018 Farm Bill. (source: The Brightfield Group)__

However, contrary to popular belief, all hemp-derived CBD products have not been fully legalized under the 2018 Farm Bill — creating uncertainty for CBD industry leaders.

Additionally, as stated in the 2018 Farm Bill and confirmed by the Food and Drug Administration (FDA), “CBD products are still subject to the same laws and requirements as FDA-regulated products that contain any other substance.”

This legal ambiguity for CBD under state and federal law has made it a “high-risk” product to many banks and payment processors, causing these organizations to suddenly and without warning drop merchant services for their CBD vending clients.

This pain can be acutely felt by CBD ecommerce store owners. While brick and mortar retailers are able to default to in-person cash payments for CBD sales, ecommerce stores have either had to resort to pay-by-check or money order payments (vastly slowing the liquidity of their revenue flow), or by contracting with expensive and unreliable “high-risk” credit card payment processors to accept online payments.

Will there be a light at the end of the tunnel for these intrepid online hemp vendors? Recent developments suggest that, very soon, the quagmire of online CBD payment processing will untangle itself as regulatory bodies relax on CBD (no pun intended).

Why CBD Banking Services are Complicated

Contrary to common belief, the 2018 Farm Bill did not fully legalize all forms of CBD nationwide. CBD can be derived from hemp, a non-psychoactive variety of the Cannabis Sativa plant.

The main difference between hemp and marijuana is that hemp contains very little THC (tetrahydrocannabinol)(0.3%), the psychoactive component of marijuana. This makes regulating hemp very tricky, since it is virtually identical to the marijuana in appearance, smell, and even taste.

1. Varying legal statuses.

Although hemp-derived CBD is generally federally legal, the laws differ in each state.

Just ask Robert Herzberg — who was transporting hemp from Colorado but was arrested on his way to Minnesota in Jackson County, South Dakota, despite the 2019 federal memorandum that prohibits states from blocking transportation of hemp. Even though Herzberg had all of the appropriate documentation for his hemp shipment, local police still confiscated it.

This discord between federal and state laws creates a risk not only for the owners of hemp businesses, but also the banking institutions that process and store revenues related to hemp.

2. High-risk valuations.

If you run a CBD business, it could be considered a marijuana-related business (MRB). With any MRB, banking institutions must subject you to enhanced scrutiny for risk assessment.

CBD and marijuana-related products are considered “high-risk” because they are part of an industry with frequent chargebacks and varying legal statuses.

As attorney William S. Hackney writes: “In reality, the chances of federal banking regulators investigating and punishing your financial institution for working with a business selling CBD products from unknown parts of the cannabis plant (especially CBD products otherwise legal under state law) is probably small. It seems difficult or even impossible to prove from which part of the plant a particular CBD product was made (labelling notwithstanding). However, those chances are not zero.”

3. Green-rush symptoms.

Banks have a tough decision to make: which CBD companies should they fund?

In this “green rush,” so many businesses have flocked to selling CBD that it is difficult to separate the model citizens from the bad actors. Companies fraudulently claiming CBD as a cure-all cultivated a financial environment with abnormally high chargebacks.

CBD Payment Processing Also Has Challenges

The main issue for CBD payment processing is vetting, as summed up in this anecdote by Beryl Solomon, CEO and founder of Poplar:

“The word on the street is that Elavon didn’t use strict enough vetting processes and illegitimate businesses made their way through. For them to stay in the good graces of the credit cards, it was easier to just drop all CBD accounts rather than to properly vet retroactively the CBD companies that they supported.”

Here are some of the biggest challenges CBD merchants face when it comes to online payment and credit card processing:

1. Lack of processors.

Only the largest payment processors have the financial leverage to stand solid against pressure from credit card companies regarding CBD sales.

Properly vetting CBD companies as clients is also a significant expense, and never fully alleviates the financial risk to payment processors.

As such, even though BigCommerce offers 60+ payment processors on its platform (making it one of the most payment agnostic ecommerce platforms currently on the market), only a handful of processors will accept payment for CBD products.

2. Lack of POS systems.

A customer pays with cash? No problem, but without Point-Of-Sale systems, many businesses cannot open brick-and-mortar shops. The logistics of conducting business solely with cash are a nightmare. Armed guards must often be on the premises to protect the large volume of cash, and armed couriers deliver cash to the few CBD-friendly banks available within driving distance.

With only physical currency at its disposal, everything financial becomes more complicated for a brick-and-mortar CBD business — payroll, inventory procurement, maintenance and other operating expenditures, etc.

3. Restrictive contracts.

If prohibition creates a black market, then the legal gray area that “protects” financial institutions providing banking services CBD transactions is creating a gray market for payment processing.

Cost of payment processing services are unusually high, with some companies charging double-digit transaction fees and requiring mandatory escrow accounts with large minimum balances. Many more of these high-risk payment processors will attach lengthy contracts that auto-renew, charging you with early termination fees along the way.

Oftentimes, these high-risk payment processors will go through foreign banks. Getting your money out from another country could mean expensive transfer fees and unfamiliar tax laws. Good luck getting your money out of a foreign country if some unforeseen circumstance arises.

CBD-Friendly Banks

Thanks to the gray market for CBD that the legal framework has created, there’s a real chance that your friendly neighborhood bank will refuse to handle any financial transactions related to CBD.

Fret not — we’ve aggregated two sample banks that represent the types of financial institutions that we believe would be amenable to CBD business transactions. Please note we do not endorse any one of the below nor do we receive any information compensation for providing this information. It is for informational purposes only.

1. Chase Bank.

Chase Bank can open its vault for CBD-related bank accounts, but will not offer its payment processing services just yet. More than likely, Chase will wait for the SAFE Banking Act or some other CBD financial services-enabling bill that will make the industry less precarious. Resourceful due to its size, Chase will also most likely wait for data to aggregate on what successful CBD companies look like in order to properly vet potential clients in the future.

2. North Bay Credit Union.

North Bay Credit Union is one of the only American banking institutions publicly admitting to handling transactions for cannabis companies, which they do confidentially for companies located in areas north of San Francisco. The credit union limits the size of the deposits that these companies can make in order to manage their capital ratios. Still, North Bay Credit Union risks federal prosecution for handling these transactions — still illegal under federal law — but serves their clients in spite of those risks.

4 Financing Options for CBD Businesses

Despite all of the challenges in pursuing a hemp CBD or other hemp-related business in a newly legalized industry, if you have the passion and persistence profit will find a way. Use these time-tested strategies that would get any business off the ground.

1. Private financing.

Do you know any angel investors or wealthy individuals that you could convince with your business plan? Professional investors most often look for other kinds of benefits in addition to common stock and can also control the valuation of your company with their investment.

That being said, most entrepreneurs in early stages of development go to their friends and family for investment. Convince your rich friends to become even richer by investing in your CBD company. You might have to jump through a few hoops or owe a couple of favors, but getting into the ground floor of a skyrocketing industry could very well be worth the hassle.

2. Starting small.

If your main concern is getting $25,000 for inventory, you may instead opt to get only $5,000 in inventory and be forced to grow slow and small (at first). If you can’t get $5,000 in inventory, maybe just try for $1,000. If you can’t get $1,000 for inventory, consider holding off until you’ve saved up a bit more funding. Even McDonald’s started with a single burger stand. Sam Parr, founder of The Hustle email newsletter, made his first small fortune selling “hot dogs as big as a baby’s arm” from a mobile cart. It doesn’t matter where your funding starts, so long as it helps gets you where you’re trying to be.

3. Saving up.

It may take you more time to jump into your business venture if you need to save up the money on your own, but you will be able to jump in without any financial commitment to a bank. Can you manage socking away ~$200/week into a standard rate savings account for six months? There’s your five grand. Saving money for an extended period of time takes discipline, but no one said starting your own business would be easy. However, there is reward in the restraint. Giving yourself six months to acquire capital provides ample time for planning CBD marketing strategies and acquiring additional research into product procurement.

4. Personal loans.

Personal loans run at a higher interest rate, but many banks offer them to you if you have good credit and proof of income. If your CBD business is a side hustle, this may be the best way to get funding. Just make sure that your business plan accounts for the interest fees so you’re not stuck in unmanageable debt. Also, CBD is still considered high-risk. Maybe don’t put your house up as collateral and, remember — personal bankruptcies stay on your credit record for 10 years.

We recommend and encourage you to be transparent and honest on any loan application as to the proposed use of the funds.

Start seeing green in your CBD ecommerce business.

Learn how you can navigate some of the unique challenges faced by CBD merchants and grow your business in our Complete Guide to CBD Ecommerce.

Don’t Lose Hope, The Future Looks Bright for CBD

Before 2018, the hemp CBD market was barely in existence in the U.S.! Imagine how much difference can be made in just one year.

So far, all but a small handful of states allow for the cultivation of hemp which opens a lot of doors to the hemp industry. Yes, working in the CBD industry is tricky right now, but big players are out there trying to sort it all out.

1. Record-setting CBD revenue.

When Wall Street starts talking, you can expect imminent legislation. As mentioned earlier in this article, the Motley Fool quotes U.S. sales of CBD products to reach $23 billion by 2023, which works out to a 107% compound annual growth rate (CAGR)!

2. Wider acceptance.

One of the main obstacles that CBD merchants are beginning to overcome is consumer education and awareness. CVS Health, Walgreens, and Rite Aid have all announced plans to carry hemp-derived CBD topicals across thousands of stores, collectively, and national grocery chain Kroger recently announced plans to sell CBD products in 17 states.

These large players have not only introduced CBD products to the mainstream population, they’ve also opened the doors for smaller companies to try their luck in the market, by increasing product availability, contributing to growing wellness trends, and supporting the proliferation of numerous product segments.

Conclusion

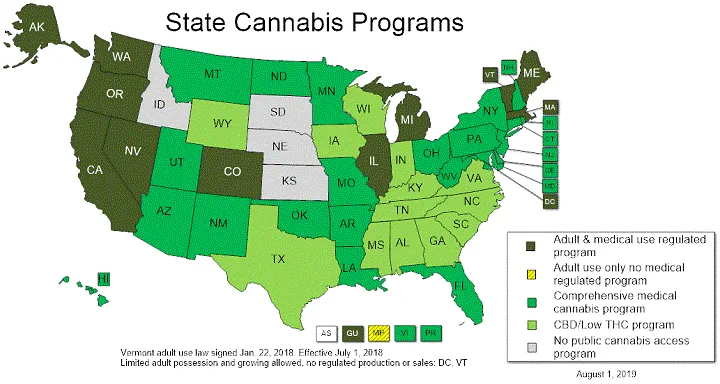

Courtesy of the National Council of State Legislatures

Medical marijuana is legal in all but four states in the United States and CBD is trending towards full, transparent legalization — not the other way around. All signs point to an inevitable, serious growth and profit opportunity in the cannabis industry.

My advice? Get educated, get funded, and get in early. One of the most exciting trends in cannabis is mergers and acquisitions. Larger, better funded companies are buying up the smaller players, making multi-millionaires out of tenderfoot tycoons — so long as their businesses represent a niche in the market that has yet to be claimed.

Please note: all references to “CBD” or “CBD products” within this post refers to hemp-derived CBD, not marijuana-derived CBD.

This material does not constitute legal, tax, professional or financial advice and BigCommerce disclaims any liability with respect to this material. Please consult your attorney or professional advisor on specific legal, professional or financial matters.